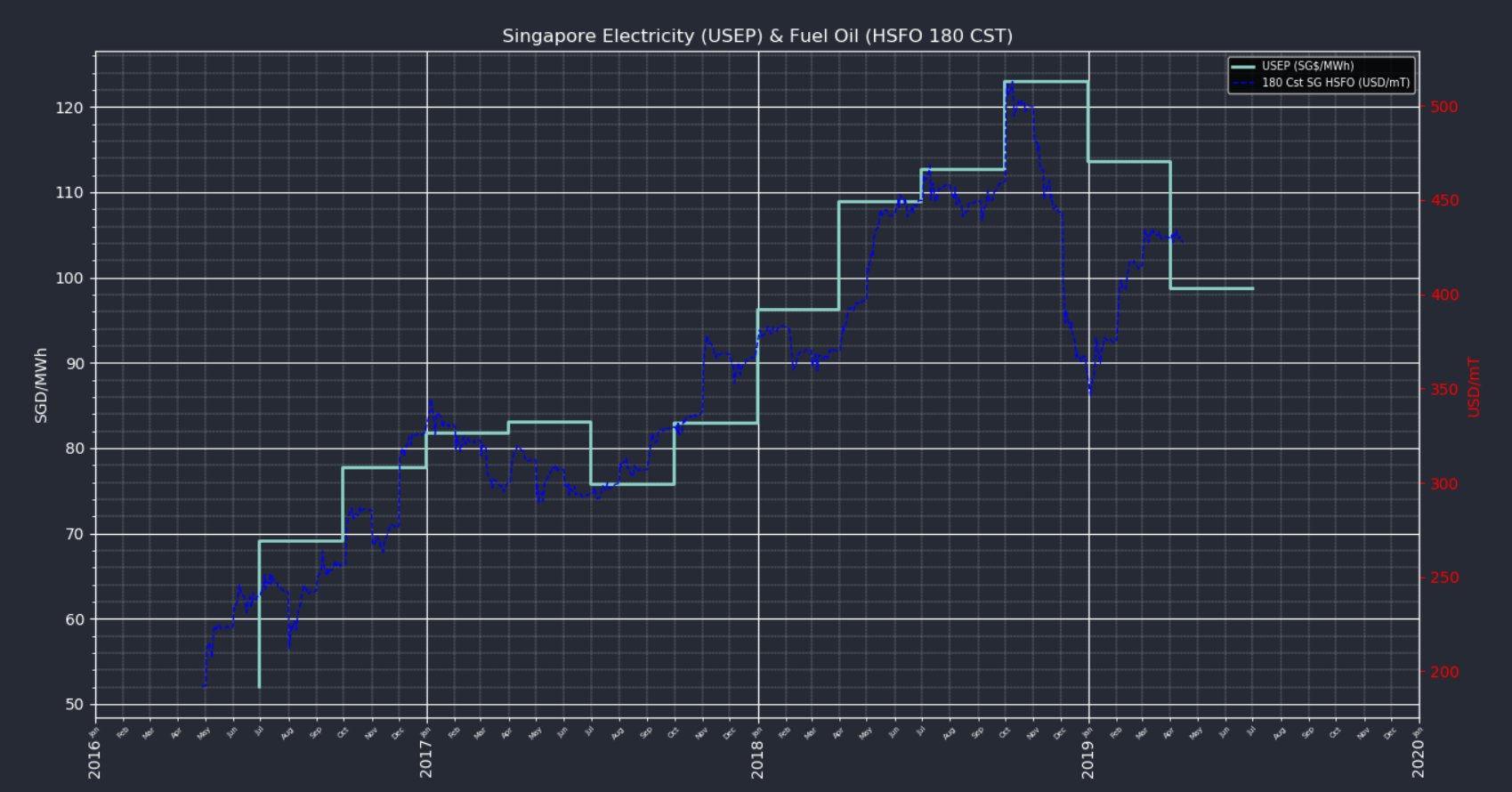

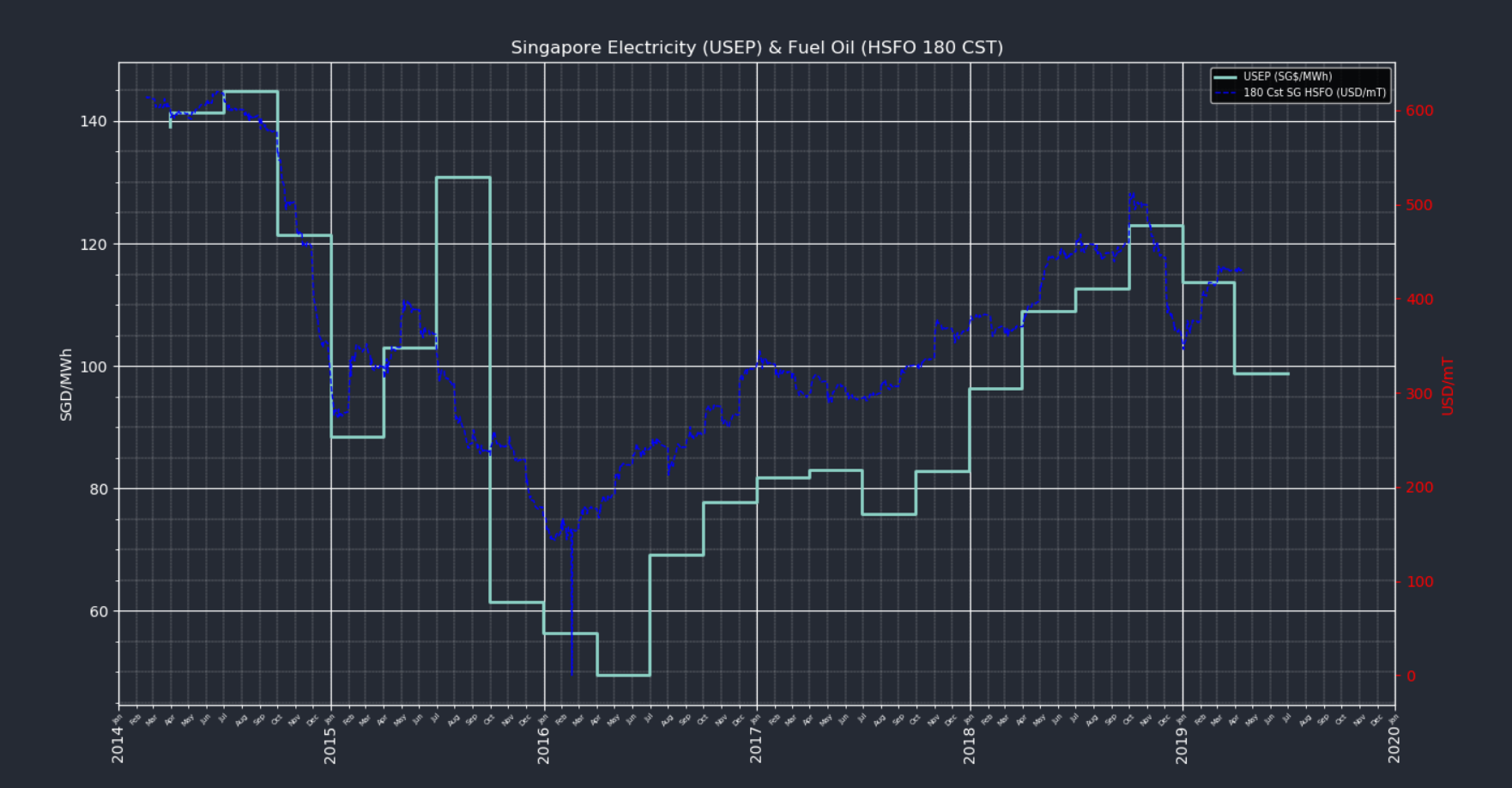

This chart shows the relationship between the USEP price and the Continuous Futures Daily Settlement Price for the Singapore 180 CST HSFO, which is an index often used in Supply and PPA contracts in the Singapore electricity market.

This chart shows the relationship between the USEP price and the Continuous Futures Daily Settlement Price for the Singapore 180 CST HSFO, which is an index often used in Supply and PPA contracts in the Singapore electricity market.

Thoughts

- Measure the co-integration z-score in order to detect for SGX trading signals

- Will an SGX product with a monthly frequency be forthcoming?

- Potentially Compare with the ACCC Netback Price Series for a more holistic view of the USEP.

A 5-Year view of the USEP historical Prices vs 180 Cst Fuel Oil Shows that the 180Cst futures price leads the NEM USEP:

Code

#Imports

import pandas as pd

import quandl

from common import common as c

#Define Time Period

begtime_str = '2016-04-28'

endtime_str = '2019-04-15'

#Get Fuel Oil from Quandl

fuelOil = quandl.get("CHRIS/CME_UA1",start_date=begtime_str,end_date=endtime_str, authtoken="<AUTH KEY HERE>")

fuelOil.rename(columns={'Settle':'180 Cst SG HSFO (USD/mT)'},inplace=True)

#retrieve USEP from previously-saved-file (or use Energy Trading API Wrapper)

df = pd.read_csv("2016to2019USEP.csv",index_col=0)

df = df[(df.index > begtime_str) & (df.index <= endtime_str)]

#get daily and quarterly averages

df.index = df.index.astype('datetime64[ns]')

pd.to_datetime(df.index)

df['dt'] = df.index.values

df['dt'] = df['dt'].astype('datetime64[ns]')

df_daily = df.groupby([df['dt'].dt.date]).mean()

df_daily.index = pd.to_datetime(df_daily.index)

df_qtr = df_daily.resample('Q').mean()

df_qtr.rename(columns={'USEP ($/MWh)':'USEP (SG$/MWh)'},inplace=True)

axis2DF = fuelOil

axis1DF =df_qtr

#Plot records

c.plot2axis2DFUSEP(axis1DF,axis2DF

,pltTitle="Singapore Electricity (USEP) & Fuel Oil (HSFO 180 CST)"

,ax1_label="SGD/MWh"

,ax2_label="USD/mT"

,ax2_list = ["180 Cst SG HSFO (USD/mT)"]

,ax1_list = ["USEP (SG$/MWh)"]

)